")

WHAT YOU NEED

TO KNOW ABOUT

YOUR CLAIM

What You Need to Know

About Your Personal Injury Claim

Being involved in a car accident can be stressful and understanding the personal injury claims process can be confusing. If you’re reading this you or someone you’re close to has likely been in an auto accident in the last couple of days or maybe even weeks, and you may be wondering what your next steps should be. We’ve written a brief article and recorded a 2-minute video explaining the 10 most important things to know and do following your accident and to protect your personal injury claim.

VIDEOS

ARTICLES

1. What is the most important thing to do immediately after an auto accident?

Safeguard Your Accident Information

- Store in a safe place the at-fault drivers information — name, address, phone number, drivers license number, and insurance information

- Keep photos of the accident scene and the damage to your car, and any other cars involved in the accident

- Be sure to have a back-up copy of the accident details, contact information, and photos on your phone, on your computer, or in the cloud

- If the information is on paper and you have printed pictures, store them with your important documents

- If there are witnesses, be sure to keep their contact information with the other information from your accident. What the at-fault driver says at the scene, may be very different from what they tell their insurance company. Witnesses make all the difference when the other driver is not being truthful about what happened.

Be Examined by a Medical Provider

If you’ve been injured in an auto accident, the most important thing is to have a full recovery as quickly as possible. Do not delay being seen by a healthcare professional. Waiting a week or longer to get treatment not only slows down your recovery time, but the insurance company will say that if you were really hurt you would’ve seen a provider immediately.

Be sure to let your providers know all of your injuries including: tingling in arms or legs, knee pain, anxiety you are having driving or being in a car, bad dreams about the accident, foggy thought process or memory problems. Even if the provider does not specialize in the areas of medicine that fits your injury — let them know. They can refer you to the right medical provider who does.

Report the Accident to Your Insurance Company

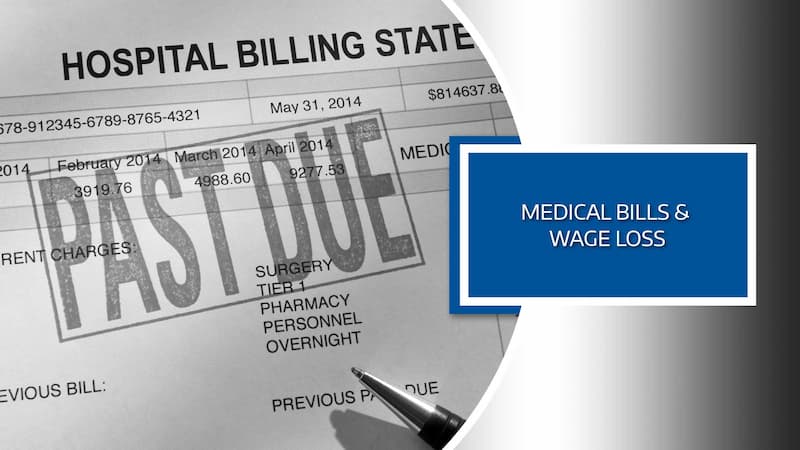

Under Oregon law, the insurance that covers the car you were injured in is required to pay all of your medical bills for 2 years or $15,000 worth of medical treatment — whichever happens first. Medical bills and wage loss are paid via Personal Injury Protection (PIP) coverage, which is a part of every car insurance policy sold in the state of Oregon.

Too often we see injured people delay or not get medical treatment because they don’t have health insurance and they don’t know about their PIP benefit that’s part of their auto insurance policy. If you have doubts or concerns that your medical bills will be paid, talk with your healthcare provider or with a personal injury attorney.

Be VERY Careful Talking with the Other Driver’s Insurance Company

While the insurance company for the driver who caused the accident does need basic information to open a claim, so the adjuster can facilitate the repairs for the damage done to your car, be aware they’re also looking for information they can use against you to prevent payouts they make on your claim. The biggest problem we see is the injured person giving more information than is needed to the adjuster. The important thing is to always keep your answers short and to the point.

The best way to protect your rights and your personal injury claim is to talk with an experienced personal injury attorney before talking with the at-fault driver’s insurance company or before giving a recorded statement.

2. Do I need a personal injury attorney if I've been involved in a car accident?

It’s best to talk to an experienced lawyer as soon as reasonably possible after your car accident. Personal Injury Attorneys offer a no-fee, no-obligation initial consultation. They will ask a variety of questions to learn more about the collision, your injuries, and the other circumstances surrounding your claim. About 60% of the people who have been injured in an auto accident do not need to hire an attorney. 100% of them find the information provided by an attorney very helpful in learning how to navigate the complexity of a personal injury claim.

When meeting with the lawyers in our firm, we will let you know if it’s not in your best interest to hire an attorney. If it doesn’t make economic sense to hire a lawyer, we are happy to provide advice and guidance so that you are in the best possible position to protect yourself and your personal injury claim. We will explain the important dos and don’ts when communicating with the insurance companies such as:

- What you should do if it’s only been a week since the car accident and the insurance company is encouraging you to settle your claim.

- What you should say to the insurance adjuster if they are asking for you to sign a medical records release authorization for the at-fault driver’s insurance company.

- If you should continue getting medical treatment for your injuries from the car accident when the insurance company is refusing to pay your medical bills.

- Your friends and family are giving you advice about your personal injury claim, and you’re wondering what really are your rights and what you should be doing and not doing to protect yourself and your claim.

3. How much will it cost me to hire a personal injury attorney?

There is no cost to talk with us or hire us — or upfront fees or costs that need to be paid, which is true for most all personal injury attorneys.

We work on a contingency fee basis. This means, if we don’t get you a settlement, you don’t owe us a fee. If your case settles without a trial, our fees are 33.33% of the settlement amount.

4. Do I have a personal injury case?

To have a personal injury claim — be it from a car accident, in a store or on someone’s property — you have to prove that the other person’s actions caused you to be injured. Usually, this means that the other person failed to drive in a way that a reasonable person does. Reasonable drivers don’t run red lights, they don’t pull out in front of another car that has the right of way, or drive so fast that they cause danger.

Claims against a grocery store for example or a claim on someone’s private property are more complex. We do represent many people injured in these types of incidents as well. If you have one of these claims, please call our office. We’ll ask you some questions to learn more about your accident and advise you on how best to proceed.

5. How are my medical bills and lost wages paid?

What is Personal Injury Protection, also referred to as PIP?

A helpful way to visualize your auto insurance policy is to think of it as a book. Books are usually divided into chapters. One of the chapters in your auto insurance book is called Personal Injury Protection. It’s like a mini health insurance policy that wraps around your car. It is required by law in virtually every auto policy sold in the state of Oregon — even if you only have liability coverage. When you and anyone in your car is injured — it is required by law that your PIP benefit pay both medical bills and wage loss. If you are in someone else’s car when a collision happens — their PIP coverage will cover you. Just like, if they are in your car, your insurance will cover them.

What are the basic PIP benefits in the state of Oregon?

- All medical expenses incurred for two years from the date of injury, up to a maximum of $15,000. The medical bills must be reasonable in amount and related to your injury from the car accident.

- Wage loss benefits of $3,000 a month or 70% of the average monthly income, whichever is less. You must be “usually engaged in paid work” and must be off work for at least 14 consecutive days.

- If you do not “usually” work, you can receive up to $30 per day for “essential services.” This benefit applies if your medical provider states in writing that you require assistance with household tasks. This, like the wage loss benefits, can continue for a total of 52 weeks. Also as with wage loss, the disability must be for at least 14 days before this benefit can be accessed. Typically the insurance company will want proof of payment for the services, including the name, address, phone number, and social security number of the person doing the work.

- If you are a parent of a minor and you are hospitalized for at least 24 hours, childcare benefits can be claimed up to $15 a day, with a maximum of $450.

- Reasonable and necessary funeral expenses incurred as a result of the accident, within one year of the accident. The minimum coverage required by law is $5000.

6. What if the driver who caused the accident does not have car insurance?

If a collision is caused by someone who does not have car insurance, your Uninsured Motorist (UM) coverage will function like the at-fault driver’s insurance company would and cover your losses from your accident, including the damage to your car, your injuries, including your pain and suffering.

Every car insurance policy sold in the state of Oregon is required to have UM coverage — even if you only have liability coverage on your policy. Uninsured Motorist coverage is one of the chapters in your auto insurance policy ‘book’.

7. How long do I have to settle my personal injury claim after a car accident?

In Oregon, the statute of limitations to settle a personal injury claim caused by an accident is two years for an adult. This means if your claim is not settled or a lawsuit is filed within two years of the collision, then all of your personal injury claim rights are lost.

For minors the statute of limitations is seven years from the date of the collision, or their 19th birthday — whichever comes first.

Another important date to consider is that there are numerous statutes that require written notice within 180 days of an injury due to an accident — such as an injury caused by a city, county, state or federal employee.

To learn more about dates critical to your personal injury claim, please read the article we’ve written about the personal injury claim statute of limitations.

8. What does the other driver's insurance company not want me to know about my rights if I've been injured in a car accident?

What’s important to remember is that the adjuster works for the insurance company. Their primary job is to protect and save money for the insurance company they work for— just like any good employee will generally do for their employer.

An adjuster is professionally trained as a negotiator. Most of us don’t have the benefit of that type of training. To best protect yourself, make sure you understand what you need to do and not do with your claim.

While you may not need an attorney to represent you, it’s really good to talk with an experienced Lawyer to get advice and guidance on how best to protect your personal injury claim. There is no fee or obligation to talk with a personal injury attorney and you are not obligated to hire them.

9. How do I find out what my personal injury case is worth?

We are often asked what is the value of a person’s claim worth who was injured in a car accident. There are many factors that go into answering that question and it’s surprisingly challenging to provide anywhere close to an accurate answer — especially before a person has finished the treatment from their injuries.

Following is a partial list of factors that go into evaluating a claim — once the person injured is “medically stationary” and has been released by their medical providers:

- Is there a question of who caused the collision?

- Has the injured person been in other accidents or have any pre-existing conditions?

- What is the visual damage to the cars involved in the accident?

- Have there been any gaps in medical treatment?

- How long did the person receive treatment for their injuries?

- Was there time loss from work?

- Who were their providers?

- What type of treatment did they receive from their providers?

- Are there permanent injuries?

- Will there be verified future medical treatment?

- What are the total costs of the medical treatment the injured person received?

- How much of the treatment has been paid by PIP and how much is owing to your providers and health insurance company?

You can see from these questions that to accurately determine a fair settlement range for a personal injury claim it is essential that the injured person has been released from their medical provider’s care.

If anyone is telling you they know the settlement value of your claim, before you are done treating, they either don’t know what they are talking about or they are not telling you the truth.

10. What is the most important thing I can do to recover from my injuries after a car accident?

First, let your medical provider know about all the injuries and discomfort you have because of the collision — even if the healthcare professional does not treat for a particular injury. When they know what all your injuries are, they’ll be able to refer you to the right provider so you can get the treatment you need. Also, if all your injuries are not properly documented in your chart notes, it can raise substantial issues as to whether it was really caused by the auto accident.

Second, tell your provider about any accidents, similar pain, discomfort, or problems you have had in the past, even if you had a full recovery. The information you give your doctor will help them to better understand your injuries and to establish the best treatment plan for you.

Don’t fall into the trap of thinking that informing your healthcare provider of prior injuries or treatment might hurt your personal injury claim. The exact opposite is true: telling your provider everything will actually help your claim. Honesty and candor are critical to a full recovery and a successful claim.

Third, make sure to follow your medical provider’s advice, including instructions on home care, and keeping your appointments.

Your goal is to have a full recovery as soon as possible. Everything you do to get better, is always what’s best for you and for your personal injury claim.

MORE PERSONAL INJURY CLAIMS RESOURCES

If You’ve Been Injured in a Car Accident

")

Top 10 Personal Injury Claim

Mistakes To Avoid

")

How Are Medical Bills

and Wage Loss Paid

After a Car Accident?

")

How to Prepare

for Your Independent Medical Exam

We are here to be a bridge of support. If you have questions about how to navigate the personal injury claim process, we're happy to talk with you. Whether you're our client or not, we want for you to get the information you need to protect your rights and your claim.

Unsure if You Have a Case?

Contact us for a NO FEE Case Evaluation

"*" indicates required fields